China reaction: Time is running out as growth slows across the board

- 16 September 2024 (5 min read)

Supply side decelerates modestly as the investment engine cools

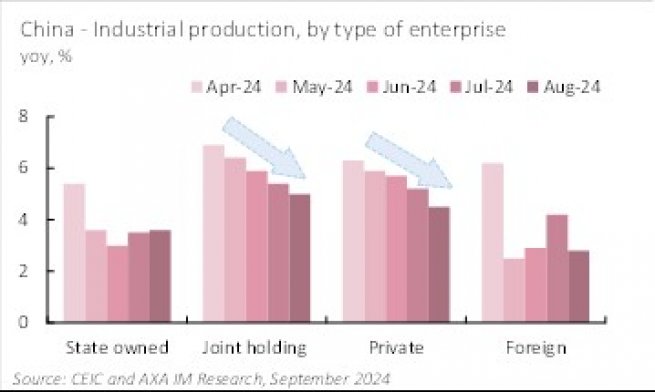

Industrial production eased further in August, growing by 4.5% on the year, 0.3% on the month (July: 5.1% yoy, 0.4% mom). The momentum in industrial production has been softening since peaking at 6.7% in April. Both joint-holding and private enterprises have seen a clear decline in production growth, with rates falling from 6.9% and 6.3% in April to 5.0% and 4.5% in August, respectively. State-owned enterprises have shown a slight recovery, with production increasing to 3.6% from the June low of 3%. Sector-wise, the decline was primarily driven by property-related weakness. Production of non-metal minerals, such as cement, and ferrous metals deepened in August, fell by 5.5% and 2.1% on the year, respectively. However, production of high-tech manufactured goods remained relatively resilient, growing by 8.6% in August.

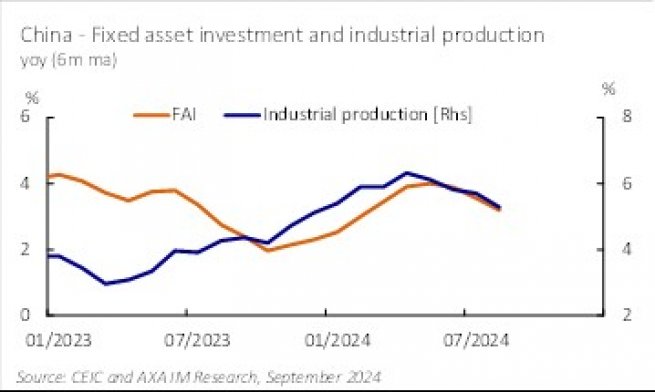

FAI continued its slowing trend, growing by 2% on the year in August, although a touch higher than the 1.9% in July. Infrastructure investment (excluding utilities) weakened further to 1.2%, down from 2% in July. Although capital investment in the manufacturing sector remained relatively strong, it followed a gradual deceleration trend, slowing to 8% from 8.3% in July. By enterprise type, FAI from state-owned enterprises and enterprises from Hong Kong, Macau, and Taiwan eased by 0.3 and 0.4 percentage points, respectively, compared to July, to 6% and 4.7%. FAI from foreign investors worsened to -17.7% from -15.2% in July. Meanwhile, private FAI narrowed its decline to -1.6% from -9.7% in July, a marked stabilisation.

Following the supply-centric stimulus measures since last year, non-property FAI has been the backbone of economic growth, closely correlating with trends in industrial production. However, as investment has softened in recent months, industrial production has also lost momentum. While the manufacturing sector has shown resilience in both investment and production growth, its strength is insufficient to offset the drag from other sectors, particularly the property sector.

Several factors may explain the slowdown in state-led investment. These include delayed bond issuance, likely due to limited project pools given various restrictions on local government bond usage; the already strained local government balance sheets and rising debt burdens; and the "lifetime accountability" of local governors, which may have made them more hesitant to engage in radical investment. The clear disconnect between central and local governments may be increasingly responsible for fractures in policy transmission.

Another weak month for domestic demand amid worsening asset price and labour market

Retail sales weakened to 2.1% on the year and -0.01% on the month in August, down from 2.7% yoy and 0.27% mom in July. Sales for consumer goods softened to 1.9% yoy from 2.7% in July, while catering edged up slightly to 3.3% from 3.0%. The trade-in programme may have boosted home appliance sales, reversing a decline to grow by 3.4% in August from -2.4% in July. However, automobile sales continued to fall, deepening to -7.3% from -4.9% in July, marking the sixth consecutive month of decline.

The persistent weakness in domestic demand results from continued asset price corrections and a bleak labour market. Property prices accelerated their fall in August, with prices for both new and existing homes extending declines by 0.1 percentage points to -0.7% and -0.9% mom, respectively, recording their 15th and 16th consecutive monthly declines. Additionally, the labour market saw a higher jobless rate in August, as the urban surveyed unemployment rate rose to 5.3% from 5.2% in July. While data limitations obscure the true state of China's labour market, a second consecutive rise in the jobless rate indicates a worsening employment situation.

China’s domestic demand is likely to remain subdued until asset prices stabilise and/or the labour market improves. Chinese consumers have been overlooked by Beijing’s supply-centric stimulus strategy in recent quarters. Although authorities have more recently begun to shift focus toward the household sector, the measures so far been timid and insufficient to counter deeply entrenched pessimism. The ongoing lack of domestic demand is pushing the economy toward the brink of deflation, with both headline CPI and core inflation remaining very weak.

Time is running out to achieve growth target

The August data release has reinforced the pessimistic outlook for China's economy, yet there is still no clear sign of stronger stimulus. Senior government officials have continued to emphasise achieving growth targets in their recent speeches, demonstrating the authorities' commitment to the economy. Nevertheless, time is running out. As the economy remains heavily reliant on policy support, the stimulus measures expected in the coming months will be crucial. Additionally, Beijing must address the disconnect between central and local governments to ensure smooth and effective policy transmission. For this year this is a question of meeting the annual growth target – something that we doubt at this stage. However, more broadly the issue is becoming more structural with the risks of China slipping into a yawning demand-deficient deflation trap growing as we move into 2025.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date.

All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document.

Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales No: 01431068. Registered Office: 22 Bishopsgate London EC2N 4BQ

In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© AXA Investment Managers 2024. All rights reserved