Biodiversity loss: Understanding and responding to a global systemic risk

- 28 September 2022 (7 min read)

- Biodiversity loss, and measures to prevent it, bring risks for businesses and the economy – but also potential opportunities

- Investors need reliable, repeatable data to drive verifiable positive outcomes in this area while seeking financial performance. We think this is now happening

- The data is helping guide our engagement efforts and understand which firms may be most affected by this part of the transition

One of the fundamental motivations for responsible investment is to better understand present and future systemic risks. In recent years this momentum has seen climate and biodiversity emerge as key themes. Climate has understandably dominated, but we believe damage to the ecosystems that support life on land and in the oceans represents an equivalent threat to long-term economic sustainability. Importantly, we think that sufficient knowledge and tools now exist for responsible investors to start addressing this issue in their portfolios.

A good starting point is to understand how human behaviour is tipping the balance. The main driver comes from changes in land use and sea use, with supplemental but important contributions from climate change, overexploitation of natural resources, pollution and the spread of invasive species.1

As awareness of these factors has grown, so have regulatory and industry efforts to tackle the problem. The international Convention of Biological Diversity (CBD) lies at the centre of activity, helping to define the work of key corporate and financial sector initiatives. The expectation is that the CBD will be further bolstered this year by the adoption of a refreshed Global Biodiversity Framework at a key meeting in Canada this December, offering clear and actionable objectives at both government and corporate level.2

References to biodiversity are also worked into new legal standards, including the European Union’s Sustainable Finance Disclosure Regulation and France’s Energy-Climate law, and look likely in the UK.3 As with climate change, it may be that the concerted policy response motivates investors to act as much as the direct risks of biodiversity loss.

The direct economic risks are deeply concerning by themselves. The World Economic Forum has assessed that about 50% of global GDP depends on high-functioning biodiversity.4 One 2021 study found that existing natural system degradation was costing more than $5trn per year in the form of lost natural services.5 And when the World Bank examined a collapse scenario for three ecosystem services – wild pollination, tropical timber supply and marine fisheries – it found that it would cost 2.3% of global GDP annually by 2030.6

Building an investment approach

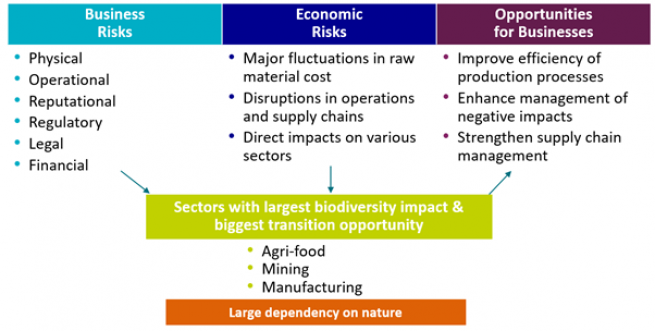

Beyond the startling global numbers, we believe biodiversity degradation brings multiple risks for businesses and the economy. The below graphic sets out some of the problems that companies may have to overcome, but also some of the potential opportunities that might arise, particularly for biodiversity leaders in the sectors most at risk – agriculture and food, mining and manufacturing.

- R2xvYmFsIEFzc2Vzc21lbnQgUmVwb3J0IG9uIEJpb2RpdmVyc2l0eSBhbmQgRWNvc3lzdGVtIFNlcnZpY2VzLCBJbnRlcmdvdmVybm1lbnRhbCBTY2llbmNlLVBvbGljeSBQbGF0Zm9ybSBvbiBCaW9kaXZlcnNpdHkgYW5kIEVjb3N5c3RlbSBTZXJ2aWNlcyAoSVBCRVMpLCAyMDE5

- VGhlIGxhdGVzdCBVTiBCaW9kaXZlcnNpdHkgQ29uZmVyZW5jZSwga25vd24gYXMgQ09QMTUsIHdpbGwgdGFrZSBwbGFjZSBpbiBNb250cmVhbCBmcm9tIDctMTkgRGVjZW1iZXI=

- VXBkYXRlIHRvIEdyZWVuIEZpbmFuY2UgU3RyYXRlZ3k6IGNhbGwgZm9yIGV2aWRlbmNlLiBVSyBnb3Zlcm5tZW50LCAyMDIy

- TmF0dXJlIFJpc2sgUmlzaW5nOiBXaHkgdGhlIENyaXNpcyBFbmd1bGZpbmcgTmF0dXJlIE1hdHRlcnMgZm9yIEJ1c2luZXNzIGFuZCB0aGUgRWNvbm9teSwgV29ybGQgRWNvbm9taWMgRm9ydW0sIDIwMjA=

- VGhlIEJpb2RpdmVyc2l0eSBDcmlzaXMgSXMgYSBCdXNpbmVzcyBDcmlzaXMsIEJDRywgMjAyMQ==

- VGhlIEVjb25vbWljIENhc2UgZm9yIE5hdHVyZSwgVGhlIFdvcmxkIEJhbmssIDIwMjE=

It’s crucial to understand how these inputs and outputs interact, to ensure when we build portfolios and invest in companies that we can understand the risk and reward, maximise the potential for alpha generation and support the economic long-term shift to truly sustainable economies.

Some of the biggest challenges for global biodiversity lie in areas such as sustainable materials, land and animal preservation, water ecosystems and recycling/recirculation – all of these areas are long-term structural growth drivers and have strong predicted market growth. We look for companies that can address biodiversity loss through mitigation and preservation and focus on finding the technologies and services that have the biggest potential impact.7

In sustainable materials, we can help mitigate biodiversity loss by finding companies that offer non-plastic packaging or perhaps that deliver alternatives to the traditional mining of lithium – an element widely used for devices such as smartphones and laptops. The traditional process produces high carbon emissions, is very water intensive and causes land degradation. So-called ‘green lithium’, however, uses a geothermal water extraction process that can help reduce harmful pollutants on land, water and air – so it can be a much cleaner process with a lower environmental impact.8

As we seek to meet our global food supply needs, we cannot escape the reality that modern animal agriculture for food production has caused significant land degradation and loss of animals, insects and plants. It represents another key biodiversity risk. Here we look at companies that are using artificial intelligence (AI), connected sensors, and emerging technologies to help the ‘precision agriculture’ industry significantly reduce the use of herbicides and pesticides. This increases the yield per acre and reduces the number of acres needed – offering gains in productivity with the same amount of land and not causing further land degradation.

The other part of the land and animal preservation opportunity is finding companies that provide plant-based alternatives; this can be anything from meat alternatives such as lab-grown products to plant-based beauty products or biodegradable textiles made from pulp and wood.

To protect water ecosystems, we can target companies active in the water management and sanitation sectors, while in recycling and recirculation we see a diverse opportunity set, including firms addressing electronic waste. Globally we produce over 50 million tonnes of electronic waste per year and only 20% is recycled.9 To meet this challenge, we are interested in companies that use vertically integrated battery material recovery processes and other solutions. The global lithium-ion battery recycling market is projected to grow to $22.8bn by 2030 – this is a compound annual growth rate (CAGR) of 19.6% by 2030.10

And we can see potential long-term growth opportunities in all the markets that we monitor as a route to mitigating and preventing biodiversity loss. In the global sustainable packaging sector, the market is estimated to reach more than $630bn by 2030 – that would represent a CAGR of more than 10%.11 It’s a similar story when we look at precision agriculture – the market was worth $5.5bn in 2021 and it is estimated to grow to $19.2bn by 2030, a CAGR of close to 15% over the period.12

Under the bonnet

This may be an exciting part of the investment universe, but if biodiversity-aware investors are to drive verifiable positive outcomes while seeking financial performance then they need one crucial thing: reliable, repeatable data. We think that is becoming a reality – with some caveats.

There are some obvious considerations: How investors get access to underlying inputs; how the tools are developed to make sense of complex compound sets of data; and defining common approaches and metrics to allow comparative analysis to track positive change. AXA IM’s partnership with Iceberg Data Lab (IDL) is designed to help overcome some of these challenges, and other initiatives are underway with providers like CDC Biodiversité and ENCORE, as well as some of the major ESG data providers.

In our view, Iceberg Data Lab offers more than that, and reports the kind of information that can inform portfolio construction and allow clear comparisons between issuers. The key datapoint deployed by IDL is known as Corporate Biodiversity Footprint (CBF) which uses as a metric ‘mean species abundance’, or MSA. This employs a life-cycle analysis model to track product flows through the value chain from sourcing to end user and examines four specific pressure points that may be a factor in biodiversity loss: land use; climate change; water pollution; and air pollution. Other inputs may be missing, such as invasive species, but we believe MSA still gives a useful estimate of the square kilometres of pristine forest that would be lost each year given the nature and impact of a company’s activities.

This assessment is integrated into our broad investment process and allows us to better understand the companies, and the sectors, that are most contributing to biodiversity loss – and perhaps facing risks as a result. Crucially, it also gives us the ability to pursue informed, active dialogue on the issue with the executive teams involved. The graphic below details our checklist for corporate engagement around biodiversity.

- VGhlIHNlY3RvcnMgcmVmZXJlbmNlZCBpbiB0aGlzIGRvY3VtZW50IGFyZSBmb3IgaWxsdXN0cmF0aXZlIHB1cnBvc2VzIG9ubHkgYW5kIGRvIG5vdCBjb25zdGl0dXRlIGludmVzdG1lbnQgcmVzZWFyY2ggb3IgZmluYW5jaWFsIGFuYWx5c2lzIHJlbGF0aW5nIHRvIHRyYW5zYWN0aW9ucyBpbiBmaW5hbmNpYWwgaW5zdHJ1bWVudHMuIE5vciBkbyB0aGV5IGNvbnN0aXR1dGUgb24gdGhlIHBhcnQgb2YgQVhBIEludmVzdG1lbnQgTWFuYWdlcnMgb3IgaXRzIGFmZmlsaWF0ZWQgY29tcGFuaWVzLCBhbiBvZmZlciB0byBidXkgb3Igc2VsbCBhbnkgaW52ZXN0bWVudHMsIHByb2R1Y3RzIG9yIHNlcnZpY2VzLCBhbmQgc2hvdWxkIG5vdCBiZSBjb25zaWRlcmVkIGFzIHNvbGljaXRhdGlvbiBvciBpbnZlc3RtZW50LCBsZWdhbCBvciB0YXggYWR2aWNlLCBhIHJlY29tbWVuZGF0aW9uIGZvciBhbiBpbnZlc3RtZW50IHN0cmF0ZWd5IG9yIGEgcGVyc29uYWxpc2VkIHJlY29tbWVuZGF0aW9uIHRvIGJ1eSBvciBzZWxsIHNlY3VyaXRpZXMu

- Q2xlYW4gRW5lcmd5IFRlY2hub2xvZ3kgSW5ub3ZhdGlvbiwgSUVBLCAyMDIy

- VU4gcmVwb3J0OiBUaW1lIHRvIHNlaXplIG9wcG9ydHVuaXR5LCB0YWNrbGUgY2hhbGxlbmdlIG9mIGUtd2FzdGUsIFVORVAsIDIwMTk=

- TGl0aGl1bS1pb24gQmF0dGVyeSBSZWN5Y2xpbmcgTWFya2V0IHdvcnRoICQyMi44IGJpbGxpb24gYnkgMjAzMCwgTWFya2V0c2FuZE1hcmtldHMsIDIwMjE=

- U3VzdGFpbmFibGUgUGFja2FnaW5nIE1hcmtldCwgTWFya2V0IFJlc2VhcmNoIEZ1dHVyZSwgMjAyMg==

- UHJlY2lzaW9uIEFncmljdWx0dXJlIE1hcmtldCBTaXplIGlzIHByb2plY3RlZCB0byByZWFjaCBVU0QgMTkuMjQgQmlsbGlvbiBieSAyMDMwLCBTdHJhaXRzIFJlc2VhcmNoLCAyMDIy

We understand that the consideration of biodiversity is at an early stage for many companies – the initial focus is driving preservation and mitigation, while biodiversity restoration will be a more important theme in the future. Our engagement is therefore focused on helping management to understand how they might measure their impact and find the key performance indicators that will allow them to first of all properly monitor the efficiency of their actions in term of biodiversity loss mitigation, and to meet regulatory demands in the future. We think our engagement is already helping identify the companies likely to be most affected as momentum around biodiversity builds and with the potential to exploit biodiversity-related transition opportunities at hand.

There may be demands on institutional investors too and it is perhaps useful to think of biodiversity being at a similar point to climate about 10 years ago. Verifiable targets will be the next, and vital, step while the escalating reach of the Task Force on Climate-related Financial Disclosures has given an indication of the expected effect of its sister initiative, the Taskforce on Nature-related Financial Disclosures (TNFD). The structure and focus of the TNFD is still in the consultation phase, and biodiversity data remains an imperfect beast, but we think major investors such as pension funds and insurers should prepare to report detail of the potential impact their investment portfolios could have on biodiversity.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.

Issued in the UK by AXA Investment Managers UK Limited, which is authorised and regulated by the Financial Conduct Authority in the UK. Registered in England and Wales, No: 01431068. Registered Office: 22 Bishopsgate, London, EC2N 4BQ. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

© 2022 AXA Investment Managers. All rights reserved