How close are we to a cashless society?

Key Points:

Cashless payments have risen rapidly in recent years, as consumers have embraced fintech solutions.

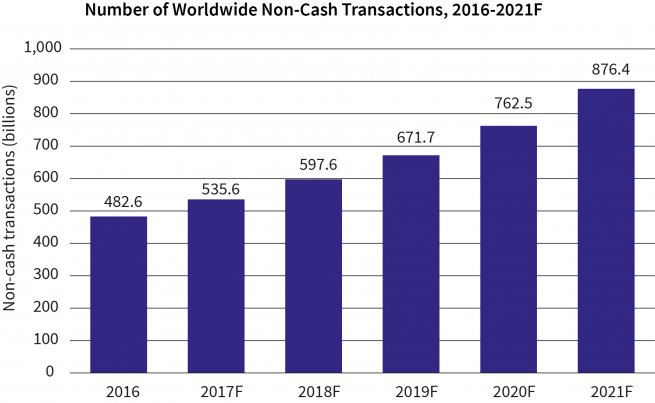

The number of non-cash transactions globally is forecast to reach 876 billion by 2021

While we do not think that cash will ever completely disappear, we believe there is a strong growth trajectory towards the cashless society.

In 2018, Chinese mobile payment providers Alipay and WeChat each processed more payments in a single month than PayPal’s $451 billion for the whole of 2017

This is a prime example of fintech’s coming of age, and goes a long way in illustrating how the emergence and development of digital technology has transformed the way that consumers pay for goods and services. In an ever-changing world where electronic payments are becoming commonplace, consumers increasingly expect quick, easy and secure alternatives to cash that they can access at their convenience.

The introduction of contactless technology in 2007 has already gone a long way to satisfying consumer demand: over the past decade, we have seen a variety of contactless-enabled payment innovations emerge, from mobile phones to smart watches, fitness trackers, wristbands, fobs and stickers.

With widespread adoption of digital payment methods in recent years, how close are we to a cashless society?

A long (but worthwhile) journey towards cashless adoption

It is clear that countries active in the adoption of digital payment methods have benefited as a result: for consumers, paying for goods and services has become a much simpler and efficient process, while businesses have a more streamlined way of processing transactions. Banks also benefit from lower costs associated with the printing, storage and transportation of cash in circulation. As technology becomes more advanced, financial institutions, as well as traditional businesses, will need to adapt to the demands of the digital age.

Sweden leads the charge towards a cashless society

Much of Sweden’s success in going cashless has come down to having trust in the fact that digital payments can be made anywhere – so much so that cash researchers Niklas Arvidsson and Jonas Hedman of the Copenhagen School of Economics estimate that cash will no longer be used in Sweden by March 2023.

In the 10 years dating back to the start of 2009, the amount of cash in circulation in Sweden has fallen by almost 40%

Legacy issues mean the US is playing catch-up

As a significantly larger, older and more complex market than somewhere like Sweden, the US is playing catch-up on the adoption of cashless infrastructure. While US banks were able to issue contactless-enabled cards by late 2016, they opted to save roughly 35 cents on the cost of manufacturing each card by issuing traditional debit cards instead.

However, US banks are finally starting to adapt to the changing technology and, with it, consumer sentiment is improving around digital payments. For example, JPMorgan announced its plans to roll out contactless technology on its payment cards by the end of 2019

Rapid expansion of mobile payments in China

Having taken a different approach to the US, China finds itself miles ahead in its trajectory towards a cashless world and, perhaps, emphasises the need to take a more aggressive approach in adopting cashless technology. Aside from rapid urbanisation, the Chinese government has recognised the need to build world-class infrastructure and fully commit to electronic payments over physical cash.

The emergence of mobile payments technology has seen innovative apps, such as Alipay (created by Alibaba in 2004) and WeChat Pay (Tencent Holdings), come to the fore. The influence of such apps on consumers has been significant: collectively, they account for around 93% of the country’s mobile payments market

The potential reach of fintech

Sweden, China and the US are just three examples of how far the adoption of digital payment methods has come. Globally, however, the cashless story varies widely across regions, with different countries at different stages of adoption.

So, while a cashless society may feel like the future of convenience in many developed markets, this transition also has the potential to more significantly disrupt and improve people’s lives in developing markets, and among demographics which currently have less access to traditional banking services – it is estimated that more than a third of the world’s adult population make little or no use of formal financial services

Some involvement from authorities is likely to be needed to support this ongoing transition, to create and maintain the necessary financial infrastructure. Overall, we see a strong growth trajectory ahead for digital payments, supported by shifting consumer attitudes, infrastructure investment and increasing political will.

Disclaimer

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

It has been established on the basis of data, projections, forecasts, anticipations and hypothesis which are subjective. Its analysis and conclusions are the expression of an opinion, based on available data at a specific date. All information in this document is established on data made public by official providers of economic and market statistics. AXA Investment Managers disclaims any and all liability relating to a decision based on or for reliance on this document. All exhibits included in this document, unless stated otherwise, are as of the publication date of this document. Furthermore, due to the subjective nature of these opinions and analysis, these data, projections, forecasts, anticipations, hypothesis, etc. are not necessary used or followed by AXA IM’s portfolio management teams or its affiliates, who may act based on their own opinions. Any reproduction of this information, in whole or in part is, unless otherwise authorised by AXA IM, prohibited.

This document has been edited by AXA INVESTMENT MANAGERS SA, a company incorporated under the laws of France, having its registered office located at Tour Majunga, 6 place de la Pyramide, 92800 Puteaux, registered with the Nanterre Trade and Companies Register under number 393 051 826. In other jurisdictions, this document is issued by AXA Investment Managers SA’s affiliates in those countries.

In the UK, this document is intended exclusively for professional investors, as defined in Annex II to the Markets in Financial Instruments Directive 2014/65/EU (“MiFID”). Circulation must be restricted accordingly.

AXA IM and BNPP AM are progressively merging and streamlining our legal entities to create a unified structure

AXA Investment Managers joined BNP Paribas Group in July 2025. Following the merger of AXA Investment Managers Paris and BNP PARIBAS ASSET MANAGEMENT Europe and their respective holding companies on December 31, 2025, the combined company now operates under the BNP PARIBAS ASSET MANAGEMENT Europe name.