The vital role of investors in the carbon transition

- 15 July 2021 (7 min read)

Pre-COVID-19, the transition to a low carbon economy was already enjoying several tailwinds. But the onset of the pandemic has fuelled this drive as companies, governments and investors appear to have galvanised their efforts like never before in a bid to tackle climate change.

Driven by a combination of risk mitigation, increasing opportunities and a desire to be responsible corporate citizens, an ever-increasing number of firms are actively incorporating environmental and carbon reduction commitments into their business strategies.

Of the world’s 2,000 largest public companies, more than one-fifth, at 21%, now have net zero commitments, representing annual sales of nearly $14trn.1 This includes companies among the sectors that are the biggest contributors to global emissions, where firms such as BP and Shell have set net zero targets.2

Industries such as automobile makers are also transforming their product offering, with the likes of Ford and Jaguar Land Rover committing to having all-electronic ranges in the next decade.3 With almost 1.4 million electric and hybrid vehicles registered in Europe during 2020 - 137% more than in 2019 - and global sales overall increasing to 3.24 million, compared to 2.26 million in 2019, manufacturers are attempting to stay ahead of the curve and keep up with rising consumer demand.4

Policy, investor, and consumer demand

Alongside companies, policymakers are also taking decisive action and governments worldwide have been upping their game with net zero announcements from China, Japan, and South Korea. In addition, some 37% of the European Union’s €750bn recovery fund will be invested in projects that support climate objectives.

Vitally, the fight against global warming is back on the agenda in the world’s largest economy, as almost immediately after taking office US President Joe Biden reinstated climate change as a major priority and re-joined the Paris Agreement.

| Environmental urgency has strengthened with COVID-19 | |

|

Governments

|

Corporates

|

|

Consumers

|

Investors

|

All in all, according to the Energy & Climate Intelligence Unit’s most recent study, countries with net zero targets together now represent 61% of global emissions, 68% of global Gross Domestic Product (in purchasing power parity terms) and 52% of the global population.5

Large asset owners are also making greater commitments towards sustainable investing – the Principles for Responsible Investment (PRI) initiative, a United Nations (UN)-supported network of investors, now has some 3,000 signatories, which collectively representing more than $100trn in assets under management.6

And asset owners are increasingly working together by partnering in alliances such as the Net Zero Asset Managers initiative, which has pledged to support the goal of net zero greenhouse gas emissions by 2050 or sooner. Presently the organisation has 73 signatories, of which AXA IM is a founding member.7

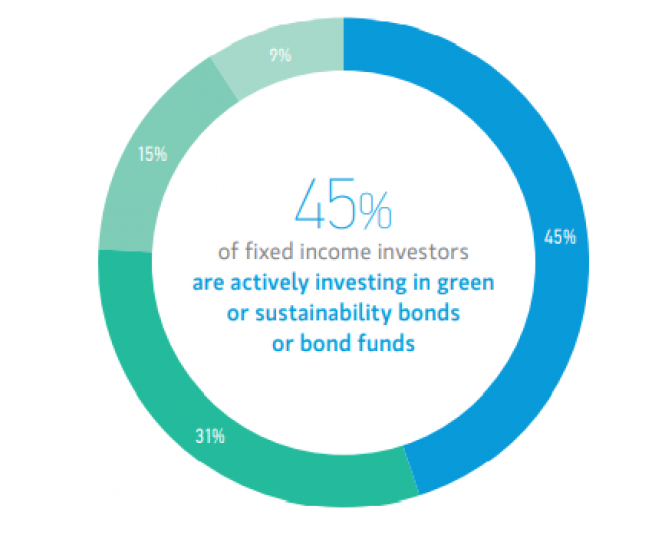

There are numerous studies showing that our clients today, and in the future, increasingly want their investments to be not only financially rewarding but also responsible. And tellingly, the popularity of responsible investments didn’t fall by the wayside during 2020, as over the year in the US sustainability-focused funds attracted more than $51bn in net new money – a new record and more than twice 2019’s total.8 In addition, sustainability strategies available to European investors attracted net inflows of €233bn, nearly double that of the previous year.9

- aHR0cHM6Ly9zdXN0YWluYWJpbGl0eS5mYi5jb20vRW5lcmd5ICZhbXA7IENsaW1hdGUgSW50ZWxsaWdlbmNlIFVuaXQgfCBFQ0lV

- aHR0cHM6Ly93d3cudGhlZ3VhcmRpYW4uY29tL2J1c2luZXNzLzIwMjAvYXByLzE2L3NoZWxsLXVudmVpbHMtcGxhbnMtdG8tYmVjb21lLW5ldC16ZXJvLWNhcmJvbi1jb21wYW55LWJ5LTIwNTA=

- Rm9yZCB0byBnbyBhbGwtZWxlY3RyaWMgaW4gRXVyb3BlIGJ5IDIwMzAgLSBCQkMgTmV3cw==

- RVYtVm9sdW1lcyAtIFRoZSBFbGVjdHJpYyBWZWhpY2xlIFdvcmxkIFNhbGVzIERhdGFiYXNlIChldi12b2x1bWVzLmNvbSk=

- RW5lcmd5ICZhbXA7IENsaW1hdGUgSW50ZWxsaWdlbmNlIFVuaXQgfCBFQ0lVIC8gRmlmdGggb2Ygd29ybGTigJlzIGxhcmdlc3QgY29tcGFuaWVzIG5vdyBoYXZlIG5ldCB6ZXJvIHRhcmdldCwgbmV3IHJlcG9ydCBmaW5kcyB8IEJsYXZhdG5payBTY2hvb2wgb2YgR292ZXJubWVudCAob3guYWMudWsp

- UFJJIGFuZCBXQkNTRCBqb2luIGZvcmNlcyB0byBkcml2ZSBjb3Jwb3JhdGUtaW52ZXN0b3IgYWN0aW9uIG9uIHN1c3RhaW5hYmxlIGRldmVsb3BtZW50IHwgTmV3cyBhbmQgcHJlc3MgfCBQUkkgKHVucHJpLm9yZyk=

- TmV0IFplcm8gQXNzZXQgTWFuYWdlcnMgaW5pdGlhdGl2ZSAtIEhvbWU=

- U3VzdGFpbmFibGVfRnVuZHNfTGFuZHNjYXBlXzIwMjEucGRmIChtb3JuaW5nc3Rhci5jb20p

- U3VzdGFpbmFibGUgRnVuZHMnIFJlY29yZC1CcmVha2luZyBZZWFyIHwgTW9ybmluZ3N0YXI=

Practical portfolio application

As an asset manager it is essential that we build and deliver investment strategies with transparent environmental targets and for several asset classes, it’s already possible to build lower carbon portfolios today.

However we believe it’s vital to create products which focus not only on companies with business models that explicitly support a low carbon economy, such as renewable energy or battery technology, but also include firms in sectors that currently have a high carbon footprint such as transport.

Many such firms, dubbed transitioning companies, are taking climate risk seriously and are actively moving to reduce their carbon footprint. Ultimately carbon emissions from all kinds of economic activity need to be reduced or offset.

Important considerations in managing portfolio data

Importantly, there has been an explosion of environmental, social and governance (ESG) data - particularly climate-related – over recent years, so access has vastly improved. But the key is being able to understand the data and make investment decisions based on it. For example, we use multiple providers for a variety of climate-related data but more significantly we are creating our own framework to have a holistic set of climate key performance indicators.

The UN Sustainable Development Goals (SDG) framework is increasingly used by investors, including ourselves. And while it wasn’t originally designed for investment purposes, we believe it’s a very useful lens to ensure we create positive and measurable impact, and so an increasing number of our strategies explicitly target alignment with several SDGs.

Investment or divestment is another key consideration. Our approach is to have engagement as one of our key pillars of our approach to responsible investing. Simply divesting from all polluting companies isn’t going to resolve the challenges we face - on the contrary, it’s crucial that we proactively engage with companies. Climate change is the number one of seven key themes which we engaged with companies on - and in 2020 it covered nearly one third of our engagement activities. We also believe that collaborative engagement is in some cases a more powerful tool so some of our climate-related engagement is done via our membership of certain industry bodies, such as the Climate Action 100+ initiative.

Impact with equities

There are several approaches investors can take when looking to allocate capital to support the transition to a lower carbon economy. One that we feel is particularly relevant for equity investors is to consider strategies which not only aim to generate positive financial returns but also to have a direct and positive impact on the environment. Investors can play a significant part in contributing to the reduction of global emissions by investing in best-in-class companies within the sectors that contribute most to emissions such as transport, energy production, industry.

One way we believe we can achieve this is by focusing on four key areas:

- Low carbon transport: The electric vehicle (EV) supply chain is likely to benefit from an increasing adoption rate of EVs in the coming years, through the development of long-lasting batteries, charging stations, semiconductors and connectors which can minimise power loss and support performance

- Smart energy: Digitalisation of buildings and industries, combined with the collapsing cost of battery storage and smart grid technology, is opening new possibilities for energy efficiency and renewable energies

- Agriculture and food: Companies are exploring new ways to meet the rising demand of growing populations, while limiting the use of scarce land. This creates opportunities to invest in firms that are developing food and agricultural technologies and solutions to address food waste

- Natural resource preservation: Public opinion is shifting and putting pressure on companies. Businesses which mitigate environmental damage by facilitating recycling, waste management, water treatment and reuse should, in our view, yield large net gains to the global economy.

|

Low Carbon Transport

|

Smart Energy

|

|

Agriculture & Food

|

Natural Resource Preservation

|

The rise of green bonds

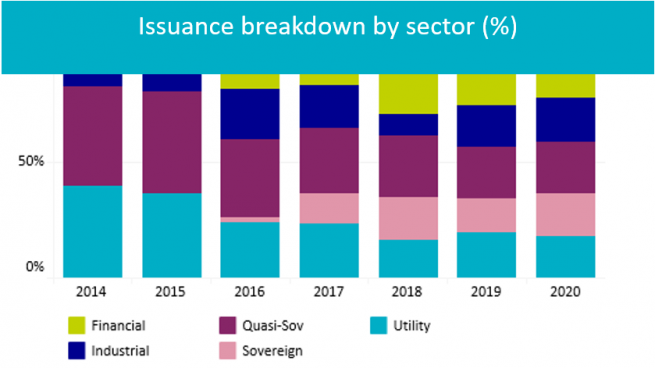

Another way to invest in the energy transition is via green bonds. The green bonds market continues to grow robustly with 2020 setting a record for issuance.10 The market is now bigger than the European high yield bond market and we are seeing increasing issuer diversification sector-wise.11

- aHR0cHM6Ly93d3cuY2xpbWF0ZWJvbmRzLm5ldC8yMDIxLzAxL3JlY29yZC0yNjk1Ym4tZ3JlZW4taXNzdWFuY2UtMjAyMC1sYXRlLXN1cmdlLXNlZXMtcGFuZGVtaWMteWVhci1waXAtMjAxOS10b3RhbC0zYm4=

- QVhBIElNLCBCbG9vbWJlcmcgYXMgYXQgMzAvMTIvMjAyMCAoR3JlZW4gYm9uZCBtYXJrZXQgZXggQ05ZLCBleGNsLiBvdXRzdGFuZGluZyAmbHQ7JDMwMG1pbyk=

Just a few years ago two areas - utilities and quasi-sovereigns - represented nearly 80% of issuance compared to less than 50% today and 2020 reflects this with increased issuance in sectors such as consumer goods, retail, telecommunications and autos, as well as sovereigns. We believe 2021 will be another record year for the market – where assets undermanagement could potentially reach $1trn.12

Green bonds are fundamentally about investing for a better, low-carbon future – as the money raised is earmarked for green initiatives. When it comes to investing in green bonds, there are two main approaches. One is to allocate green bonds into an existing fixed income portfolio and the other is to invest in dedicated green bond strategies. At AXA IM we do both, and a key ingredient to selecting the right issuers is our green bond go/no go framework. Via this tool, we analyse each green bond on four key criteria – ESG quality of the issuer, the merits of the project, the use of proceeds and how the issuer will monitor and report on the project.

- UkkgLSBHcmVlbiBib25kcyBtYXJrZXQgZXhwZWN0ZWQgdG8gdG9wIHRoZSAkMXRybiBtYXJrIGluIDIwMjEgLSBBWEEgSU0gR2xvYmFsIChheGEtaW0uY29tKQ==

The next phase

The carbon transition marks a huge structural shift in the way the global economy will operate. Investors need to think about this in the broadest sense; reducing over time their exposure to high-carbon activities and increasing their allocations to solutions that help the transition. Capital can both benefit from and facilitate the movement of all business activity to a lower carbon model.

Fundamentally, the COVID-19 crisis has accelerated this transition to a lower carbon economy and there is no shortage of climate-focused investment solutions designed to support this transformation. We believe as asset managers we have an active, and vital, role to play by investing capital to deliver financial returns and support this evolution.

Not for Retail distribution

This document is intended exclusively for Professional, Institutional, Qualified or Wholesale Clients / Investors only, as defined by applicable local laws and regulation. Circulation must be restricted accordingly.

This document is for informational purposes only and does not constitute investment research or financial analysis relating to transactions in financial instruments as per MIF Directive (2014/65/EU), nor does it constitute on the part of AXA Investment Managers or its affiliated companies an offer to buy or sell any investments, products or services, and should not be considered as solicitation or investment, legal or tax advice, a recommendation for an investment strategy or a personalized recommendation to buy or sell securities.

Due to its simplification, this document is partial and opinions, estimates and forecasts herein are subjective and subject to change without notice. There is no guarantee forecasts made will come to pass. Data, figures, declarations, analysis, predictions and other information in this document is provided based on our state of knowledge at the time of creation of this document. Whilst every care is taken, no representation or warranty (including liability towards third parties), express or implied, is made as to the accuracy, reliability or completeness of the information contained herein. Reliance upon information in this material is at the sole discretion of the recipient. This material does not contain sufficient information to support an investment decision.